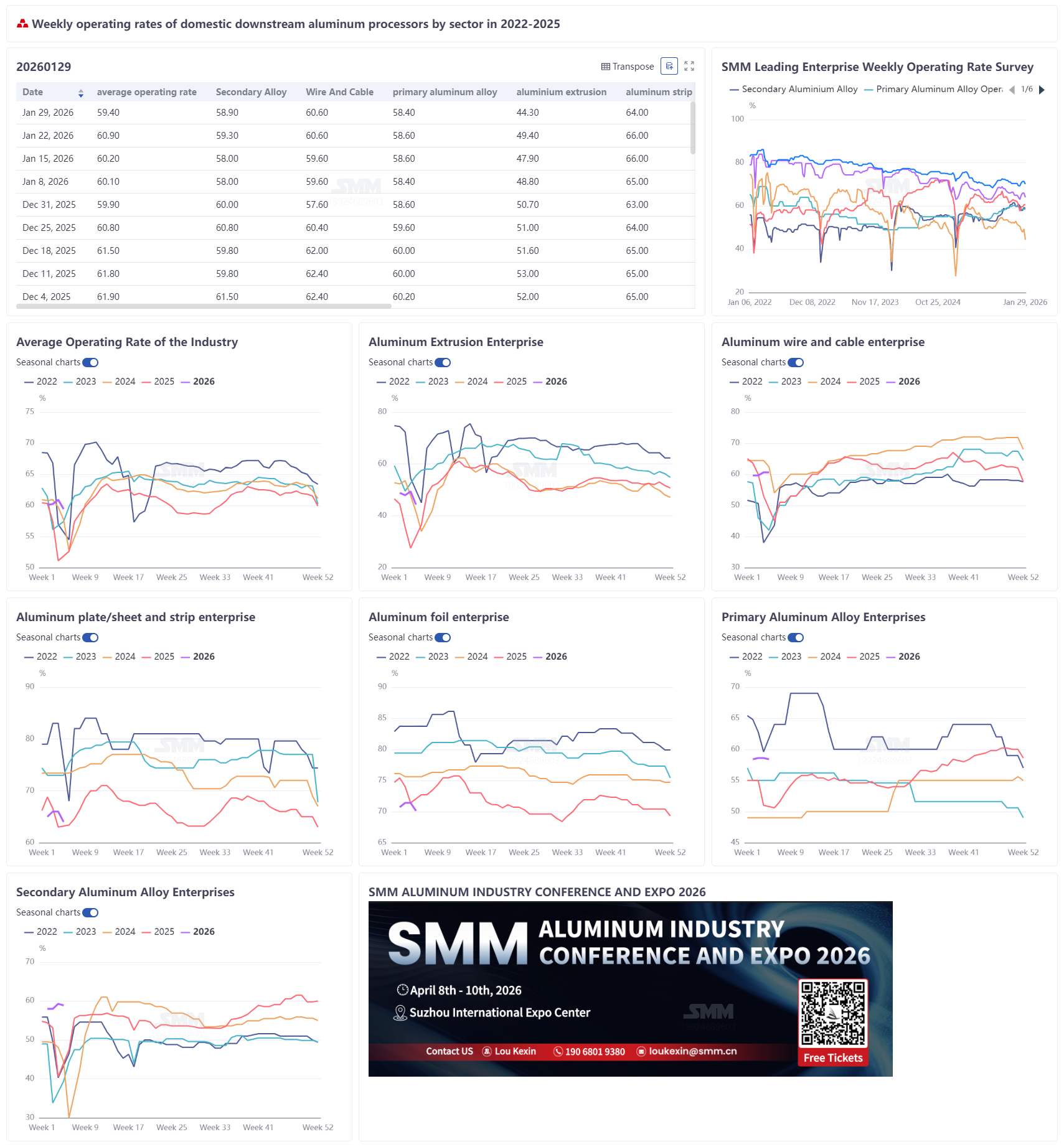

January 30, 2026:

This week, the comprehensive operating rate for aluminum processing recorded 59.4%, down 1.5 percentage points WoW, overall exhibiting the characteristics of "accelerated seasonal decline and deepening high-price suppression effects." Operating rates across most segments declined, indicating the industry is rapidly entering the off-season rhythm of the Chinese New Year. Specifically, the operating rate for aluminum extrusion was most directly impacted by the Chinese New Year break, plunging 5.1 percentage points MoM to 44.3%. Small and medium-sized enterprises in regions like Hebei and Shandong have successively halted production. Demand for construction profiles remained weak, with only orders for certain industrial materials like PV providing some support. The operating rate for aluminum plate/sheet and strip also fell 2.0 percentage points to 64.0%. A rapid price surge of nearly 1,000 yuan for aluminum during the week, coupled with repeated environmental protection-driven production restrictions in central China, severely dampened downstream stocking willingness, leading to a widespread shift to purchasing as needed. The operating rate for aluminum foil pulled back to 70.1%. While seasonal demand for traditional food and pharmaceutical foil was robust, persistently high aluminum prices continued to squeeze profits for low and mid-end products, causing customers to be cautious about cargo pick-up. The primary aluminum alloy and secondary aluminum segments continued a pattern of being generally stable with slight fall, with operating rates edging down slightly. High prices led to strong resistance downstream, and the market exhibited characteristics of "nominal prices without actual transactions." Some downstream die-casting enterprises in the secondary aluminum sector planned early holidays, further weakening demand expectations. In contrast, the operating rate for aluminum wire and cable held steady at 60.6%, performing slightly better than seasonal expectations, primarily supported by power grid orders and top-tier enterprises maintaining production to ensure post-holiday deliveries. Overall, as the Chinese New Year approaches, aluminum prices at absolute highs continue to suppress downstream restocking and stockpiling momentum, resulting in sluggish market activity outside of rigid demand. It is expected that operating rates across all segments will see a further broad decline before the Chinese New Year holiday.

Primary aluminum alloy: This week, the operating rate for the primary aluminum alloy industry edged down 0.2 percentage points MoM to 58.4%, remaining within a relatively stable, rangebound fluctuation range. Supply side, most enterprises maintained normal production, while a few slightly reduced January production plans due to weaker downstream orders. Demand side, purchasing sentiment initially recovered, boosted by the previous decline in aluminum prices. However, with the recent rapid rebound in aluminum prices, downstream fear of high prices reemerged, wait-and-see attitudes strengthened, and actual purchasing demand narrowed somewhat. Overall, the current market is generally stable with slight fall, with limited fluctuation amplitude. As the February Chinese New Year approaches, enterprise production schedules may gradually slow down. The industry operating rate is expected to show a mild pullback, with the market continuing to operate mainly in the doldrums.

Aluminum plate/sheet and strip: This week, the operating rate for leading aluminum plate/sheet and strip enterprises fell 2.0 percentage points MoM to 64.0%. Enterprise operations showed significant structural divergence: the can stock segment, due to concentrated release of rigid stockpiling demand before the Chinese New Year, saw some production lines maintaining full capacity operation, providing some support to the overall operating rate. However, overall industry order momentum was insufficient, and the core suppressive effect of high aluminum prices became increasingly prominent. The rapid surge in aluminum prices during the week, rising nearly 1,000 yuan over two days, severely impacted downstream purchasing sentiment, drastically increasing procurement pressure. Enterprises widely delayed or canceled pre-holiday centralized stockpiling plans, switching to strict purchasing as needed. This was compounded by repeated environmental protection-driven production restriction impacts in central China, causing periodic disruptions to regional enterprise production. Looking ahead, the temporary recovery in can stock demand alone is insufficient to offset the broad suppression of overall demand by high aluminum prices. Furthermore, the current absolute high price of aluminum continues to weaken downstream purchasing capacity. Against the backdrop of short-term rising aluminum prices, downstream stockpiling sentiment remains low, and the prospects for a recovery in the aluminum plate/sheet and strip operating rate are pessimistic.

Aluminum wire and cable: This week, the weekly operating rate for domestic aluminum wire and cable enterprises stabilized at 60.6%, flat WoW, showing more resilience compared to the same pre-Chinese New Year period in previous years. Driven by renewed order matching from State Grid and China Southern Power Grid, downstream production enthusiasm saw a slight rebound, with actual operating rates slightly exceeding seasonal expectations. Although it is not the peak period for power grid cargo pick-up, enterprises generally adopted an "order-oriented + post-holiday stockpiling" strategy to ensure post-holiday deliveries. Main production lines at top-tier enterprises mostly continued until the last week before the Chinese New Year, with some departments maintaining low-load operation during the holiday. The effective digestion of previous backlog orders was a key factor supporting the current operating level. As the Chinese New Year approaches and stockpiling gradually concludes, the operating rate is expected to remain in the doldrums starting next week. The pace of post-holiday work resumption, the rhythm of cargo pick-up for new energy end-users connected to the power grid, and the impact of aluminum price fluctuations on purchase willingness will be key points for the recovery of the operating rate after the holiday in February.

Aluminum extrusion: This week, the domestic aluminum extrusion operating rate was 44.3%, down 5.1 percentage points MoM. The main reason was that some sample enterprises had entered the Chinese New Year holiday period, with small and medium-sized enterprises in regions like Hebei and Shandong successively halting production for holidays, leading to a significant decline in regional operating rates. For construction profiles, demand was generally weak, and related enterprise operating rates continued to decline, with only a few large enterprises in South China maintaining relatively stable rates. For industrial extrusion, influenced by adjustments to export tax rebate policies for PV modules and batteries, enterprises in Anhui, Hebei, and Fujian reported favorable orders for PV frame and battery profiles, providing support to their operating rates. Looking ahead, some enterprises in East China and South China will gradually begin holidays next week, and the industry operating rate will continue its seasonal downward trend.

Aluminum foil: This week, the operating rate for leading aluminum foil enterprises fell 1.3 percentage points MoM to 70.1%. At the operational level, production pace for aluminum foil enterprises in the region was somewhat disrupted due to a Level I response for heavy pollution weather in central China. Combined with the impact of the significant climb in aluminum prices, the overall operational pace was cautious. Industry orders showed a stark contrast: traditional consumption areas like food packaging foil and pharmaceutical foil experienced a seasonal demand recovery, with related enterprises operating at full capacity, basically at full load, and related project orders providing stable support. Short-term, the seasonal recovery in traditional sectors and the stability of new energy demand together form a bottom support for the aluminum foil industry's operating rate. However, the negative impact of high aluminum prices is equally profound, continuously squeezing the already thin processing fee margins for low and mid-end products, leading customers to adopt more cautious cargo pick-up attitudes and more refined purchasing behavior. If aluminum prices continue to rise, it will further inhibit buyer stockpiling sentiment, significantly increasing the risk of a counter-seasonal decline in the aluminum foil operating rate.

Secondary aluminum: This week, the operating rate for leading secondary aluminum enterprises recorded 58.9%, edging down 0.4 percentage points MoM, mainly dragged down by weak demand. Under the dual pressure of high aluminum prices and the seasonal off-season, downstream purchase willingness was significantly suppressed, with market transactions mostly consisting of restocking for rigid demand. As the price center for aluminum continued to shift upwards, the characteristic of "nominal prices without actual transactions" became more pronounced, with both market inquiries and transactions noticeably cooling. Downstream pre-holiday stockpiling willingness also fell sharply, and some die-casting enterprises have clearly planned early production halts for holidays, indicating that subsequent demand will continue to weaken. Affected by factors such as successive downstream work stoppages and policy disruptions, the holiday schedule for secondary aluminum plants has been brought forward. The industry operating rate is expected to maintain a week-by-week declining trend before the Chinese New Year.|